The One Big Beautiful Bill of 2025: 5 Things Aircraft Buyers Need to Know

Jecobra Aviation is a professional aircraft brokerage that provides aircraft transaction representation and consulting. We are not qualified tax professionals. This article is for informational purposes only. Consult an Aviation Tax Expert for tailored and qualified advice.

On July 4, 2025, Congress passed the “One Big Beautiful Bill of 2025,” resurrecting one of the most prominent tax incentives for aircraft buyers — 100% Bonus Depreciation.

This accomplishment marks an inevitable seismic shift in the Private Jet market, and now is the time to educate yourself before prices go through the roof.

What Is Bonus Depreciation?

Bonus Depreciation allows businesses to immediately deduct a significant portion (or all) of the purchase price of eligible assets — including aircraft — in the year the asset is placed into service.

Prior to the “One Big Beautiful Bill”, buyers were subject to a taper down structure that only allowed partial depreciation of their aircraft (2023: 80%, 2024: 60%, 2025: 40%, etc.)

The 2025 bill increases that percentage to 100% for both new and pre-owned aircraft, as long as aircraft owners meet certain business-use criteria and place the aircraft into service within the same tax year.

That means, for example, if a business owner acquires a $10 million jet after January 19th, 2025 and uses it for qualifying business purposes, they could potentially deduct the entire $10 million from their taxable income.

Here are five things to know before you embark on the journey of acquiring a private jet and reaping the benefits of 100% Bonus Depreciation

5 Things Aircraft Buyers Need to Know Before 2025 Ends

1. Immediate Impact on the Market

Brace for impact – Aircraft buyers now have a much more compelling financial incentive to accelerate aircraft acquisitions. With an influx of motivated buyers entering the market, inventory is likely to dwindle, and aircraft values to increase.

2. Increased Dealflow Puts Pressure on MROs

At Jecobra, we often see tax related acquisition timelines come to fruition in Q4. This seasonal surge in transactions puts pressure on MRO capacity, making it increasingly difficult to secure slots for Pre-Purchase Inspections.

As a result, buyers may face a logistical risk of missing the critical deadline to place the aircraft into service before December 31, or compromising the recommended caliber of PPI.

3. Service Date Matters

It is important to note that by virtue of the transaction closing does not meet IRS criteria for “placed into service”.

The aircraft must take a flight for qualified business purposes in the tax year that you intend to take bonus depreciation as well.

Yet again, this may become a logistical issue if the aircraft is not delivered and placed into service in that tax year to claim that year’s deduction.

4. More Than 50% Business

When consulting with clients about their mission, the question often comes up: “If I purchase an aircraft and intend to claim 100% Bonus Depreciation, can I still use this aircraft for personal trips?”

The short answer: yes, you can, but in order to defend your bonus depreciation:

- The total usage for the aircraft in a given fiscal year must exceed 50% business use

- Personal and entertainment flights are not tax deductible for the business

- Personal flights may require imputations for each passenger and are subject to income tax

Personal and entertainment flights on a business aircraft may be subject to income imputations under certain circumstances. Income imputation refers to the value that must be included in an employee’s income for personal use of a company-provided aircraft, which is determined using either the fair market charter rate or the Standard Industry Fare Level (SIFL) method.

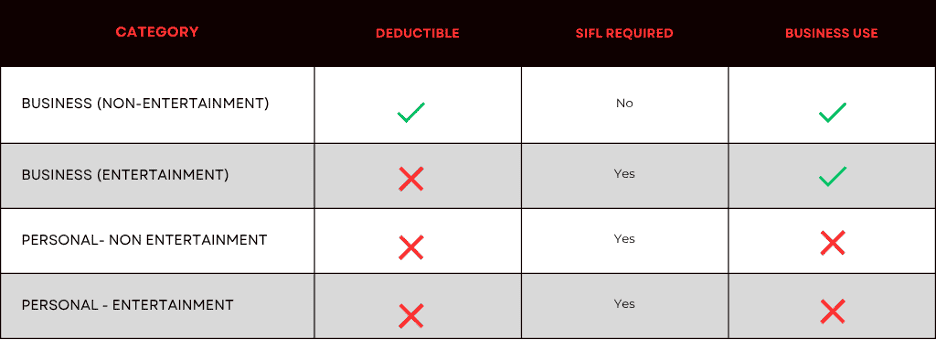

SIFL is a per-mile rate set by the U.S. Department of Transportation and updated quarterly. It’s used by the IRS to determine how much value a passenger received when flying on a company aircraft for personal reasons — and how much income should be reported on their W-2. Let’s take a look at the SIFL categories to better understand how each flight should be properly documented.

- 1. Business Use (Non-Entertainment) – Flights conducted primarily for business purposes, such as meetings with clients, visiting facilities, or attending industry events. These flights are fully deductible and do not require SIFL computations. To reiterate; more than 50% of the aircraft’s total usage must fall under this category to qualify for bonus depreciation.

- 2. Business Use (Entertainment) – This category defines flights that further a legitimate business purpose but are classified by the IRS as “entertainment” — such as taking clients to a sporting event or company retreat. Although flights that fall under this category may be incidental to your business, certain expenses may be subject to disallowance under IRC §274 and still require SIFL imputation for passengers.

- 3. Personal (Non-Entertainment) – This category defines flights that are related to personal reasons that are not incidental to furthering the business.

- 4. Personal (Entertainment) – This category defines flights for personal entertainment reasons, such as travel to vacations, sporting events, concerts, etc.

It is important to note that company executives or employees may legally utilize the business aircraft for personal trips, so long as the trip expenses are imputed according to SIFL criteria and the value is reported as income due to the fact that those passengers received value from the company that did not come out of their own pockets.

To defend your depreciation claim and stay compliant with IRS rules you must:

- Document every leg of every flight — including date, origin/destination, passengers onboard, and purpose of the flight.

- Categorize each flight as business, personal, or mixed-use.

- Run and retain SIFL calculations for all personal use by executives or employees.

This documentation is essential not just for IRS audits, but for substantiating your bonus depreciation claim. If the IRS determines the aircraft was used primarily for personal or entertainment purposes — without proper income imputation — you could lose the entire deduction.

We recommend all aircraft-owning businesses:

- Use digital flight log tools (we use Airplane Manager).

- Assign a tax advisor or internal controller to review logs monthly and verify accurate SIFL categorization.

- Ensure the aircraft operating entity has written policies for personal use, W-2 imputation, and SIFL compliance.

5. Reselling Your Aircraft After Taking Bonus Depreciation

What happens if you want to sell your aircraft after claiming 100% Bonus Depreciation?

If you resell your aircraft after taking bonus depreciation, you become subject to “Depreciation Recapture”. Recapture is a tax mechanism that allows the IRS to “recapture” the benefit you received from previously claimed depreciation deductions when you sell the asset for more than its book value.

If you take 100% bonus depreciation in Year 0, the aircraft’s tax basis becomes $0 immediately. So if you sell the aircraft in Year 1, the entire sale price (up to your original cost basis) is treated as recaptured depreciation. This amount is taxed as ordinary income, not capital gains. Any amount received above the original purchase price would be taxed as capital gain. Selling soon after purchase may result in a large tax liability, even if bonus depreciation was used upfront.

Recapture is triggered no matter how long you’ve owned the aircraft, even if it was disposed of at a loss.

Final Thoughts: A Legacy That Lives On

100% Bonus Depreciation is a revolutionary incentive for business owners to acquire and operate private aircraft. It is a testament to the American spirit and our culture’s never ending pursuit for growth and innovation.

The first introduction of 100% Bonus Depreciation yielded staggering spikes in transaction volume and the private aircraft market thrived. It democratizes access to aircraft ownership for a new class of entrepreneurs, catalyzes the pre-owned jet market, and positively influences how buyers structure their flight departments.

At Jecobra, we help clients navigate the aircraft acquisition process with clarity — including when and how to leverage depreciation to their advantage.

Have questions about buying an aircraft before year-end?

We’re happy to walk you through the tax and timing considerations to make sure you’re covered — and compliant.